Category: Innovation, Intrapreneurship, Metrics

Jan 22

Risk Calculation for Intrapreneurial Projects

The basic problem with every innovation is forecasting revenues. Intrapreneurs may know to some level of certainty how much it will cost to reach a certain stage with their project, but it’s nearly impossible to predict how the success on the market will be.

While there are a series of metrics to measure innovation, management – and especially the finance department – will ask questions on the monetary impact in order to approve the project. Ignoring those questions and not giving revenue forecasts may not be garnering the necessary management support. Even that we have talked in the past about the micro versus macro-scale innovation evaluations approach, it may be a good strategy to provide revenue metrics and come up with an ROI figure.

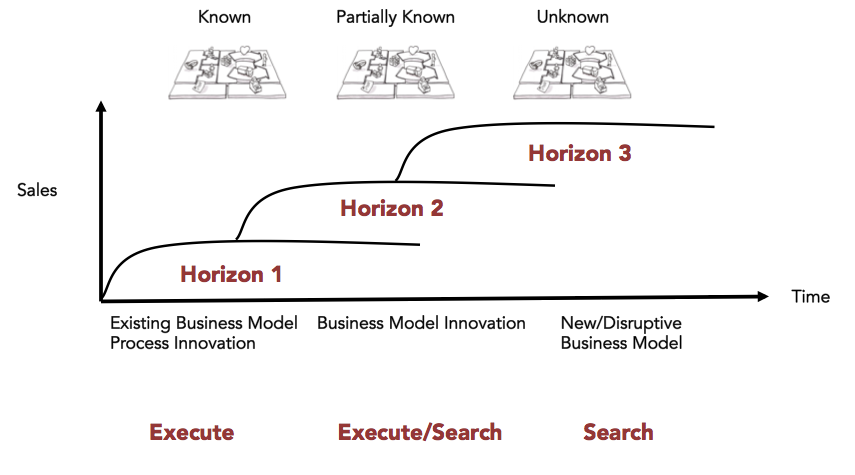

But we have to understand that the financial metrics that corporations ask for are mainly based on Horizon 1 of the Three Horizons of Growth. In this stage with an existing business model everything is more or less known.

Intrapreneurs are in Horizon 3, where everything is unknown and uncertain. The risk is high, but the payoff as well. While in Horizon 1 the metric to focus is on profit, Horizon 2 growth, Horizon 3 requires to focus on costs.

| Share | People | Metrics | Systems | |

| Horizon 1 | 70% | Managers | Profit | Robust |

| Horizon 2 | 20% | Leaders | Growth | Fragile |

| Horizon 3 | 10% | Innovators | Cost | None |

Luckily, intrapreneurs don’t have to look far to find a helpful tool. Angel investors and VCs use a financial model, that helps investment managers to hedge the financial risk of a portfolio with options. An option is the right – but not the obligation – to buy or sell a security in the future for an agreed price. Options are a widely used tool and you may have used one yourself when buying a house and you locked the mortgage.

This model can be applied to innovation and hedge against the innovation risk. Instead of handing down all the money at once for an innovative project, every phase is evaluated and the project continued with more money released or terminated. Like in venture financing an intrapreneurship project goes through several iterations. You start with a smaller amounts and go through the phases. At each phase investors can decide whether to continue with the project or shut it down.

David Binetti who lent that model from the financial world called the application to intrapreneurship Innovation Options.

How does it work?

An intrapreneur must know three things for the calculation of innovation options:

- Main investment budget: how much will the new product cost, including development and marketing?

- Best-case scenario: what’s the best-case scenario for the market potential?

- Options terms: what’s the duration and evaluation interval?

Those three values then go into the options formula that simulates three outcomes at every stage:

- good

- indifferent

- bad

What we get is a pricing tree that determines the terminal value for each possible outcome, and sums up the discounted expected values of those outcomes into a specific valuation at that point. David Binetti leads us through such an example in his blog post.

Once applied we can easily see how we start out with a valuation 6.5 million dollars and because things went well, the stage 2 evaluation (2nd quarter) shows a value of 17.8 million dollars. While the third quarter kind of side-stepped, the project is still positive and gets a thumbs up to continue.

Here you can find an online tool that allows you to calculate ROI and the risk of pre-growth (Horizon 3) initiatives.

Advantages

There are some additional advantages for such a model. Instead of providing just one traditional NPV, each stage comes with a pricing tree. At every stage the progress can be evaluated and poured into numbers that make it easier for decision making.

Considering the risk sigma, we’ll find that

- the metrics are normalized.

- innovation projects become comparable.

- it enables corporate governance.

The more stages we put in, the lower the risk sigma. Of course the more stages we build in, the more effort we put on progress reporting, which can refocus resources from market testing to spending too much time on reporting.

Other advantages come for the KPIs. They

- show sensitivity and specificity (accuracy).

- bring us fall out, miss rate, PPV, or FOR.

- allow clinical trials for the business model.

Limitations

This model is limited to work for market risk. The product or service must already be in a stage that it can be tested in the market.

- Lean startup/process is addressing the market risk.

- Agile startup/process is addressing the development risk.

We also need to understand that valuation is NOT a KPI. It’s comparable to life-insurances. You wouldn’t cancel a life-insurance because you accrued only costs in the past periods and didn’t have any payouts. In fact, in Horizon 3 stages the vast majority of options are never exercised. Most ideas never go anywhere and need to be cancelled. That’s how innovation works. Nine out of ten startups fail. The same is true with corporate innovation.

Unfortunately, we tend to manage companies just with KPIs that stem from Horizon 1. This makes corporations vulnerable to failure. But with Innovation Options we give corporate intrapreneurs and management a tool to better evaluate the success and risk of innovation.

Recent Comments